Nuveen: Implications of the Dutch pension transition

With almost € 2 trillion of pensions assets on the move, the Dutch pension transition is raising fundamental questions for pension providers. What are the implications for different asset classes?

By Gül Poslu, Managing Director, Head of Benelux, Global Client Group, and Asbjörn Friederich, Senior Research Analyst, both at Nuveen

By January 2028, approximately € 1.8–1.9 trillion in pension assets – an amount equivalent to approximately 150% of Dutch GDP – must transition from the old FTK framework to the new Wtp system. This is one of the most significant pension reforms in the Netherlands’ history.

New system, new investment philosophy

The recent research paper ‘A new investment landscape: implications of the Dutch pension transition’ from Nuveen explores what this transition means for pension providers. It explains why the move to the new regime requires a fundamental shift in investment philosophy for pension providers. In this article, we focus on the asset-class-specific implications. The paper discusses these in more detail and provides further insights into the new system.

Three regulatory changes will drive changes in asset allocation:

- The introduction of age-based lifecycle risk profiles, which replaces the previous system’s one-size-fits-all positioning;

- The elimination of punitive VEV capital charges on risky assets;

- The adoption of market-based risk assessments to replace prescribed regulatory shocks.

These changes require pension funds to pivot away from the old system’s predominantly risk-averse approach. It allows for more return-seeking investing appropriate for those in early and midstages of their working lives.

Under the old FTK system, pension funds had to maintain buffers to ensure 97.5% certainty of paying all benefits within a single year. This forced uniform positioning across all participant age groups regardless of their retirement horizon. It effectively penalised returnseeking behaviour through VEV capital charges on equities and illiquid assets, making risk-bearing investments artificially expensive to hold.

The new Wtp system removes these constraints. The changes mean that investment decisions can now be driven by expected returns, observed risk characteristics and participants’ investment time horizons. We therefore expect higher equity allocations for younger cohorts and a greater role for real assets, private markets and illiquidity premiums across pension portfolios.

Capital reallocation underway

Essentially, assets and strategies that were previously considered too high risk under the old system are now being reconsidered. As a result, significant reallocation is expected as pension providers comply with the changes.

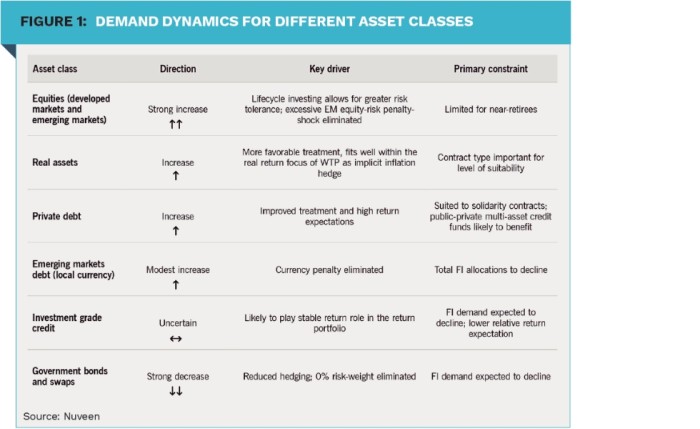

We expect substantial increase in equity allocations. Funds are targeting considerably higher equity allocations for younger participants, driven by lifecycle implementation and the VEV capital charge elimination. Developed market (DM) equities are likely to be the single largest beneficiary. But emerging markets (EM) equities should also gain given the elimination of the 40% regulatory shock (versus 30% for developed markets), which removes a 33% penalty. As revealed during our research interviews, pension funds are also looking to reposition regional exposures amid ongoing geopolitical uncertainty, which will likely be expressed in global equity portfolios.

Among fixed income assets, demand for government bonds and interest rate swaps faces structural decline. AAA-rated government bonds move from regulatory favourites in the old system to a neutral assessment in the new. At the same time, interest rate hedging requirements will decline dramatically, with approximately € 100-150 billion in long-end government bond sales expected.

Within the remaining, smaller fixed income allocations, our research suggests composition will likely shift to returngenerating spread products, such as emerging markets debt, investment-grade credit and high yield.

Opportunities in real assets

Infrastructure, real estate and broader real assets should benefit from the different regulatory treatment of riskier assets, with a less-penalising risk classification in the new system. They also offer diversification opportunities from the increasing equity allocations, with meaningfully lower volatilities than equities. Furthermore, they have the potential to protect portfolios from inflation, often through contracted cash flow agreements. The need for preserving purchasing power was highlighted by many investors in our research, supporting our expectations that allocations to real assets, including farmland and timberland, will increase.

While decisions to add new private asset classes or make sizeable allocation changes will take time, pension funds that transitioned in January 2026 are expected to begin making such changes around the second and third quarters of 2026. More funds will pursue private assets in 2027 after transitioning. According to our research, private debt is under active investigation by multiple pension funds, with implementation expected primarily from 2027 onward. Pension portfolios can now gain exposure to attractive illiquidity premiums given the improved regulatory treatment and new contract design (solidarity contracts, the most popular type under the new regime), which can accommodate illiquid investments.

Demand for ESG and impact investing

Another change with the new Wtp system is that participants are likely to be asked about their preferences for investing along sustainability and impact lines. And pension plans will need to accommodate these preferences. Fortunately, many of the regulatory changes will help facilitate the increasing interest in sustainabilityfocused and ESG investing.

By allowing for greater risk tolerance and higher-risk assets, portfolio exposure to corporates will increase, through equity and corporate bond allocations, as well as real assets, private credit and private equity. By providing capital in these different investments, investors have different avenues to influence corporate policies. This may be partly facilitated by any increase in active investing, but we think the use of benchmarks with ESG, impact or sustainability criteria is also likely to increase as a consequence.

A successful transition

This article highlights the major supply and demand implications for different asset classes as a result of the pensions transition. From our research, we also conclude that success requires understanding how lifecycle mechanics drive these allocation changes and also how contract structure will determine implementation.

|

SUMMARY By 2028, €1.8–1.9 trillion in Dutch pension assets will shift from the FTK to the Wtp, requiring a fundamental investment rethink. Lifecycle investing replaces uniform allocation as risk becomes age-dependent, and the removal of VEV charges and regulatory shocks enables more return-seeking strategies. Equities, private assets and real assets gain importance, while government bonds and hedging demand decline. ESG and impact investing expand, driven by participant preferences and greater investment freedom. |